Sometimes, bad news is good news. History says that’s the case for the recent string of high-profile bank failures.

Over the past two weeks, the banking sector has imploded.

Silicon Valley Bank failed first. Days later, Signature Bank collapsed. Those were the second- and the third-largest bank failures in U.S. history. Then a week later, it looked like First Republic (FRC) and Credit Suisse (CS) were going to fail, too. But bigger banks saved them from collapse with massive cash infusions.

The banking sector is melting down right now.

Most investors are freaking out about this meltdown, and reasonably so. After all, banks are the heart of the global economy. If they’re failing, that’s not a great sign for the economy.

But oddly enough, it is a great sign for the stock market.

Bank Failures Are a Buy Indicator

Did you know that bank crises tend to mark the end of bear markets and the start of new bull markets?

It’s true. They’re the ultimate contrarian buy indicator.

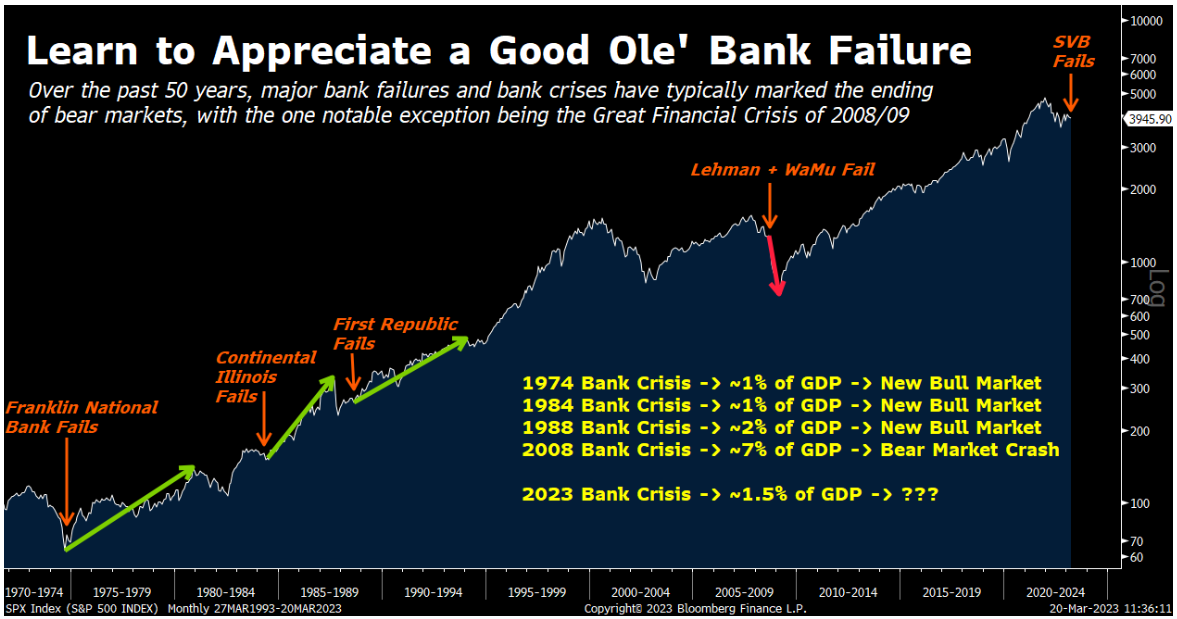

The 1974 bear market ended when New York’s Franklin National Bank went under in October 1974. That very same month, a nasty bear market (in which stocks dropped nearly 50%) ended. Over the next six years, the stock market soared 125% higher.

The 1984 stock market crash ended when Continental Illinois – a huge bank with over $100 billion in inflation-adjusted assets at the time – failed in May of that year. Over the next three years and change, the market powered more than 100% higher.

The 1987/88 stock market crash ended in the summer of 1988, when both First Republic Bank and American Savings & Loans failed – two banks with combined inflation-adjusted assets of about $150 billion. Over the next year, stocks jumped 35%. Over the next five years, they soared about 70%.

Time and time again, bank failures have marked the ending of bear markets and the start of new bull markets.

Why does this happen?

Because bank failures are usually the last domino to fall in an economic crisis.

Banks don’t just suddenly fail. They fail after months and even years of economic hardship burdening their assets and customers. They fail when an economic crisis is already in its final innings. They don’t fail in the top of the first.

Why Are Bank Failures Bullish?

Importantly, when banks do fail, the government usually comes to the rescue. And when the government starts rescuing things, economic crises usually end, and recoveries usually begin.

That is, when a big bank goes under, the U.S. government starts to worry about systemic risks to the financial system. So, it rushes to patch up the bank failure’s damage. It bails out the depositors, works to get the bank bought out, cuts interest rates, or creates emergency lending programs. In other words, it begins stimulating the economy.

And when the government starts stimulating the economy, the economy starts to recover.

Indeed, bank failures are usually very bullish for stocks because they signal impending government stimulus, which helps stem economic demise and promote an economic recovery.

The only exception is the 2008 financial crisis. Bank failures in the summer of 2008 led to a big stock market crash – not a rally. But the difference is size. In the 1974, 1984, and 1988 banking crises, the total assets in the failed banks measured about 1% to 2% of U.S. GDP. In 2008, the total assets of the failed banks measured more than 7% of GDP. It was a much bigger failure and, therefore, required more time to fix.

Outside of the anomalous GFC, though, bank failures have pretty much always signaled bear market endings and bull market beginnings.

{kind=link}

Therefore, the question is whether or not the current banking crisis is more like 1974, 1984, and 1988, or 2008?

We believe it is far more similar to 1974, 1984, and 1988.

2023 Bank Crisis: The Start of a New Bull Market

That is, the combined assets at Silicon Valley Bank and Signature Bank at the time of their failures measures about 1.5% of total U.S. GDP. Even if you assume First Republic goes under along with a few other regionals, we’re still likely only talking about 2% of total GDP in failed bank assets in 2023.

That’s in-line with the 1974/84/88 standards of 1% to 2% and well-below the 2008 high of over 7%.

This isn’t a repeat of 2008. It’s a repeat of 1974,1984, and 1988. And in each of those instances, bank failures marked the turning point from a stock market crash to a rally.

We are at that turning point now.

In response to the recent string of bank failures:

- The U.S. government has said it will possibly provide insurance for all deposits over $250,000 at all banks if systemic risks emerge.

- The U.S. central bank created an emergency funding facility for banks.

- The Swiss central bank poured $50 billion into Credit Suisse.

- Central banks across North America and Europe announced expansion of their collective emergency funding facilities.

- The Bank of Canada has paused its rate-hike cycle.

- The ECB has adopted a “wait-and-see” approach to its rate-hike cycle.

- The Fed is likely to execute its final rate hike today.

The Final Word

The writing is on the wall, folks. Governments and central banks across the globe are swiftly riding to the rescue of troubled banks. Operation “Save the Banks” has begun. Operation “Save the Economy” has begun.

And operation “Save the Market” has begun, too.

Why else is the stock market up 4% since the bailouts began last week? Why else did stocks soar yesterday?

The smart money recognizes the huge opportunity that is presenting itself today in stocks, and they’re capitalizing on it.

You should, too.

But you shouldn’t capitalize on it by just buying an ETF that tracks the S&P 500.

Rather, you should buy the individual stocks that will lead this coming new bull market breakout.

Luckily, we’ve analyzed tons of data and conducted rigorous quantitative analysis to find these breakout stocks.

You can find out about those market-leading stocks right here.

On the date of publication, Luke Lango did not have (either directly or indirectly) any positions in the securities mentioned in this article.