Sometimes, the best thing an investor can do to protect their portfolio is to sell an overpriced stock. Knowing which dividend stocks to sell is just as important as knowing which ones to buy. Holding onto overpriced or risky investments can drag down your overall returns in the long run.

It’s important to be proactive with your investments and be ready to sell any stock that may no longer belong in your portfolio. Whether due to declining performance, financial instability, or shifting market dynamics, identifying the right time to sell certain dividend stocks can help with your investment strategy and long-term goals.

No category of dividend stocks is more pertinent than real estate investment trusts (REITs). These bundled investing vehicles rely on several outside factors like prime interest rates and the housing market to remain solvent Thus, when their incomes and dividends decrease it can be a signal to exit.

AGNC Investment (AGNC)

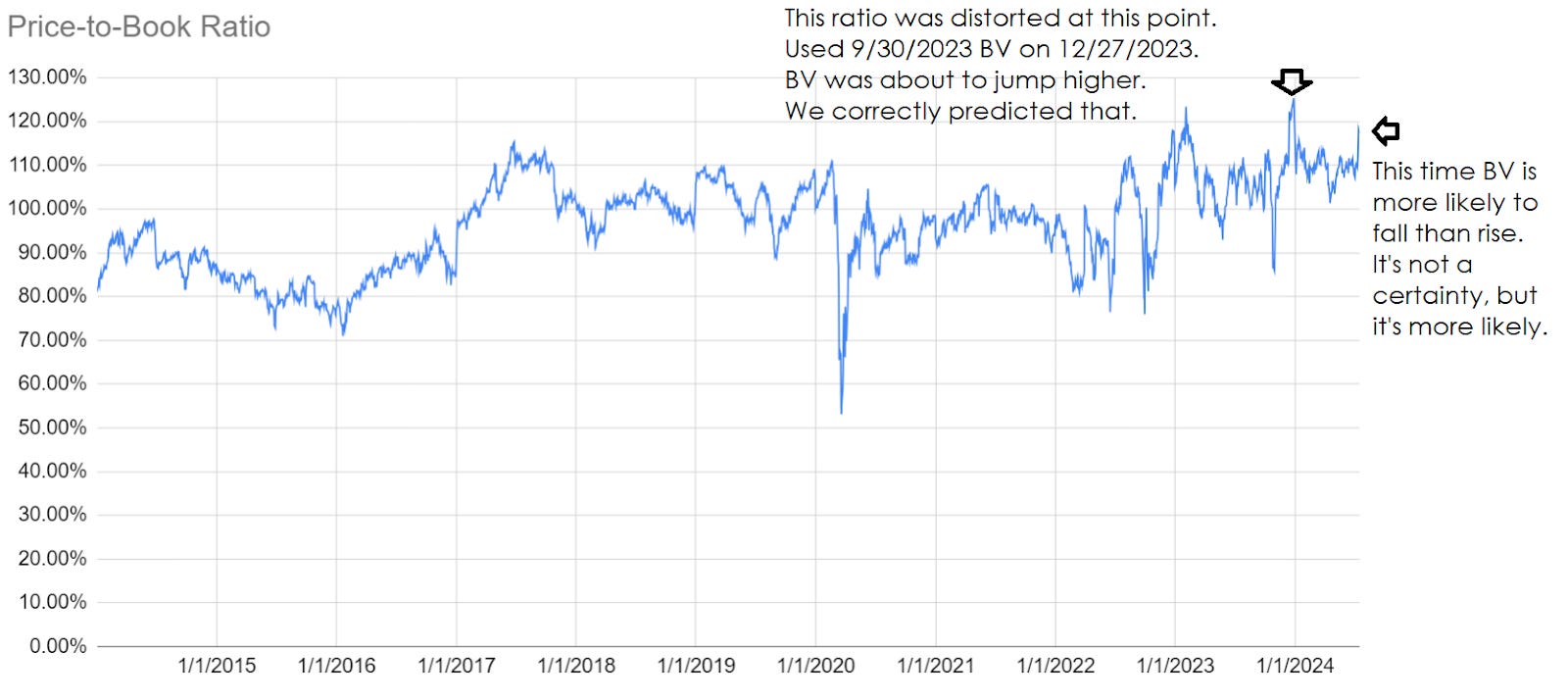

AGNC Investment (NASDAQ:AGNC) is a mortgage REIT currently offering a dividend of around 15%. Investors considering mortgage REITs should know that book value plays an important role in share valuation. A major aspect of researching mortgage REITs is examining the book value relative to the current stock price. This is known as the price-to-book ratio. It is also important for investors to compare the company’s ratio to peers.

For Q2, AGNC reported a book value of $8.40, down from $8.84 in the previous quarter. The recent price of AGNC’s stock was $10.00. Using AGNC’s reported book value for Q2, the price-to-book ratio is 1.19. Since the ratio is over 1.0, AGNC would be considered to be trading at a premium. Such a large premium for AGNC is somewhat unusual.

Investors may be asking: is there a reason for such a large disparity in price-to-book ratios among peers or compared to AGNC’s historical values? Not a good one, as AGNC is significantly overpriced and thus one of the dividend stocks to sell.

{kind=link}

Digital Realty Trust (DLR)

Digital Realty Trust (NYSE:DLR) is a data center REIT in a booming sector.

As a data center REIT, investors believe DLR will be part of the AI boom. DLR’s share price certainly benefited, but there hasn’t been much else going right. Growth in revenues is driven by growth in shares outstanding.

There has been zero dividend growth since early 2022, yet the dividend yield is only 3.3%. DLR is priced for growth, but delivering.

In the Q2 earnings update, DLR shared just how much the sector was booming. On the 3rd page of the presentation, you can see that the sector vacancy rates are trending down. Over a 3-year period starting in 2020, global data center vacancy went from 10.8% to 6.5%.

You may be thinking that sounds really good. You would be right, but not for DLR. DLR’s occupancy was 86% in late 2020, which can be found on page 45 of its 2020 investor presentation. Since occupancy was 86%, vacancy was 14%.

Readers are probably assuming that DLR’s vacancy rates also fell. They did not. At the end of 2023, DLR’s vacancy rate was at 18.3% which you can find on page 14 of its Q4 investor presentation.

ARMOUR Residential REIT (ARR)

ARMOUR Residential REIT (NYSE:ARR) is a mortgage REIT that I believe is currently overpriced. For the quarter, ARR isn’t doing as well as its peers when it comes to book value. Book value for Q1 was $22.07 for ARR. ARR reported a book value at $20.30 for the second quarter. This was a painful 8% decline.

The REIT Forum predicted book value would fall to $20.65, so $20.30 was about 1.7% lower than expected.

Even though ARR’s book value decreased, its earnings went up. For Q1, earnings came in at $1.008. For Q2, earnings came in at $1.076. Because earnings did go up, I would only consider this a slight underperformance for ARR.

The thing investors like about ARR is the huge 14% dividend yield. They may even assume that the dividend is thoroughly covered. It looks that way because ARR’s annualized dividend is $2.88. That seems “safe” when the consensus earnings figure is $3.73. However, ARR’s earnings and dividends have consistently declined when measured over long periods. Some quarters are good, some are bad, and some are even awful.

It’s the nature of how the portfolio is built. ARR owns agency MBS (mortgage-backed securities) and hedges the assets with LIBOR swaps and futures contracts. These hedged portfolios perform best when interest rates are stable. If rates rise or fall significantly, the gains on one side of the portfolio are usually smaller than the losses on the other.

On the date of publication, Michael VanLoon did not hold (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.

On the date of publication, the responsible editor did not have (either directly or

indirectly) any positions in the securities mentioned in this article.